The Beneficiary Check Most Families Put Off Too Long

A life insurance policy pays the people named on the form, not the people named in a conversation. A short beneficiary review can prevent a painful surprise later.

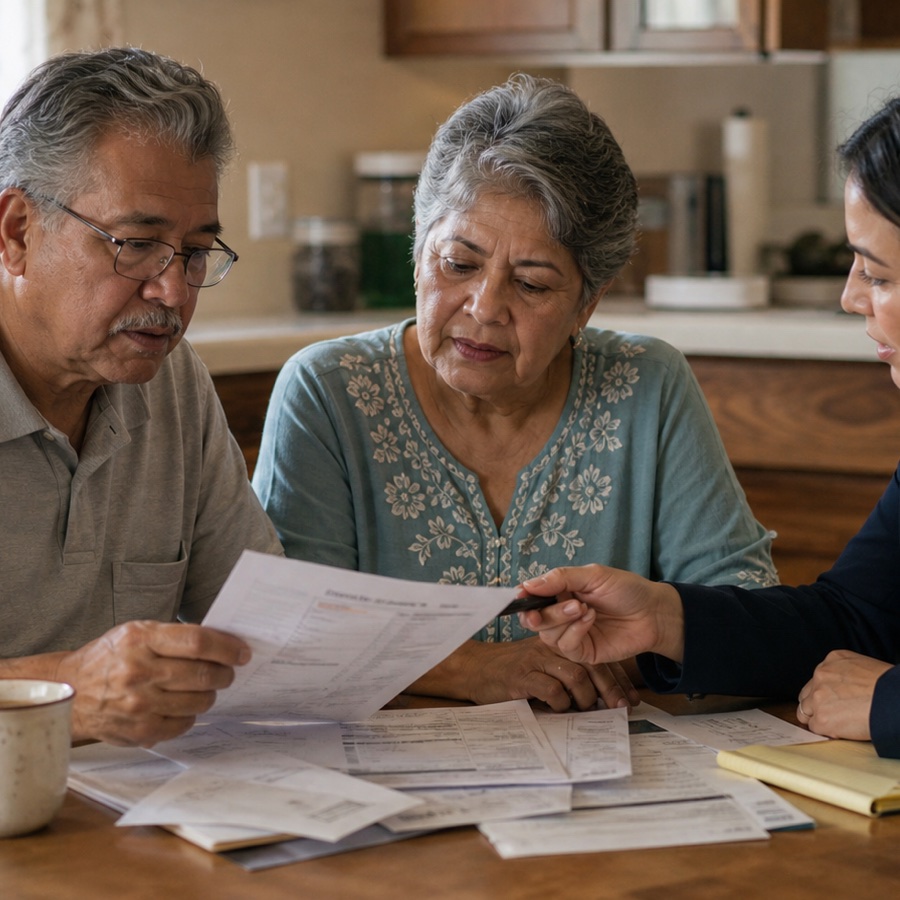

Covers policy renewals, final expense questions, auto and home coverage, and plain-English checklists for readers 55+.

Why beneficiary forms go stale

Policies are often bought decades before they pay out. Marriages, divorces, remarriages, births, deaths, and estrangements all change who a policyholder would choose today. The insurer follows the written designation, so an out-of-date form can send money to a former spouse or leave out a grandchild the family assumed was included.

- Review beneficiaries after any marriage, divorce, birth, adoption, or death in the family.

- Check both the primary and the contingent (backup) beneficiary.

- Confirm names, spellings, and relationships match current reality.

Ask how the money would actually be split

If more than one person is named, ask the insurer whether the policy splits the benefit per person or per family branch. Those rules change what happens if one beneficiary dies before the policyholder. A licensed agent or the carrier’s service line can explain the current designation in plain language.

A life insurance policy pays the people named on the form, not the people named in a conversation.

Minors and special situations need extra care

Insurers generally cannot pay a benefit directly to a minor child. Naming a minor without a custodian or trust arrangement can delay the payout. Families supporting an adult with a disability should also ask a qualified professional how a direct payout could affect needs-based assistance before naming that person.

Keep the paperwork where family can find it

A policy only helps if someone knows it exists. Keep the carrier name, policy number, and agent contact with your other important papers, and tell one trusted person where they are. If a family believes a deceased relative had coverage no one can locate, state insurance regulators offer a policy locator service that searches participating insurers.

Where to verify this yourself

These official and consumer-protection sources cover the programs and rules discussed above. Rules change, so check the current version before acting.

Was this checklist useful?

One anonymous answer per reader. Results guide the editorial desk and are not displayed publicly until enough real votes exist.