Term or Whole Life After 55: What Each One Is Actually For

The two main kinds of life insurance solve different problems. Knowing which problem you are solving makes every quote easier to judge.

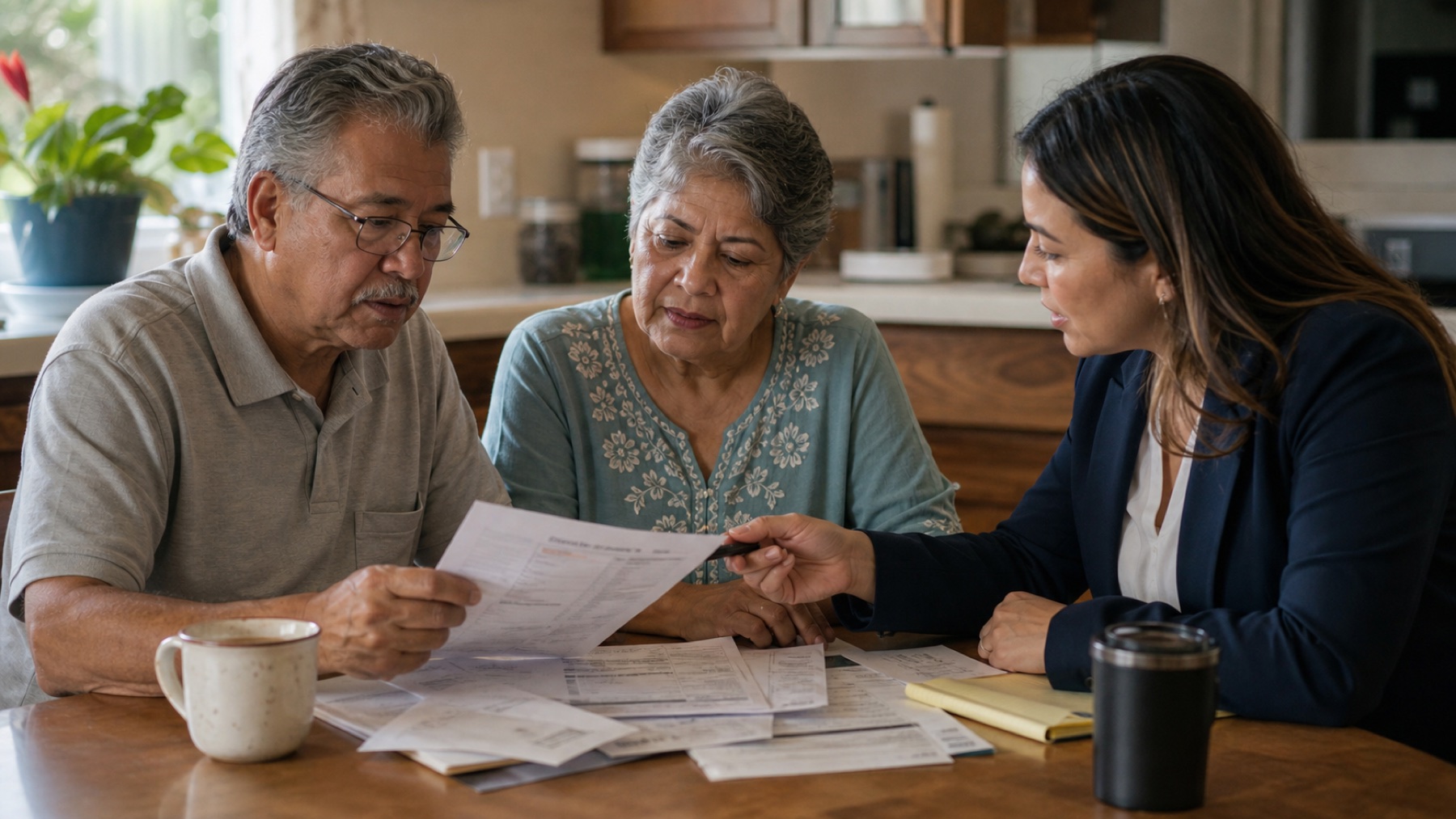

Covers policy renewals, final expense questions, auto and home coverage, and plain-English checklists for readers 55+.

Term insurance covers a period of time

Term life pays only if death happens during the chosen term, such as ten or twenty years. It is generally the least expensive way to cover a debt or income need that will end, like a remaining mortgage. After 55, the tradeoffs are that new terms cost more, health questions matter more, and renewing after the term can be expensive or unavailable.

Permanent insurance is designed to last a lifetime

Whole life and other permanent policies are built to stay in force as long as premiums are paid, and many build cash value. Premiums are higher for the same death benefit. Small permanent policies are what most final expense ads are selling, which is why the details in the fine print matter so much.

- Ask whether the premium is level for life or can increase.

- Ask whether the death benefit is fixed or graded during the first years.

- Ask what happens to the policy if a payment is missed.

Knowing which problem you are solving makes every quote easier to judge.

Match the policy to the actual need

A household with a mortgage that ends in twelve years has a different need than a household that mainly wants funeral costs covered. Writing the need down first — the amount, and how long it lasts — turns a confusing sales conversation into a simple comparison.

Be careful replacing coverage you already have

Replacing an older policy restarts waiting periods and contestability windows and can raise the premium for the same benefit. A legitimate reviewer should compare the old policy side by side with the new one and explain, in writing, what is gained and what is lost.

Where to verify before you sign anything

Every state has an insurance department that licenses agents and carriers. Checking a license is quick and free, and state consumer guides explain policy types without a sales agenda.

Where to verify this yourself

These official and consumer-protection sources cover the programs and rules discussed above. Rules change, so check the current version before acting.

Was this checklist useful?

One anonymous answer per reader. Results guide the editorial desk and are not displayed publicly until enough real votes exist.