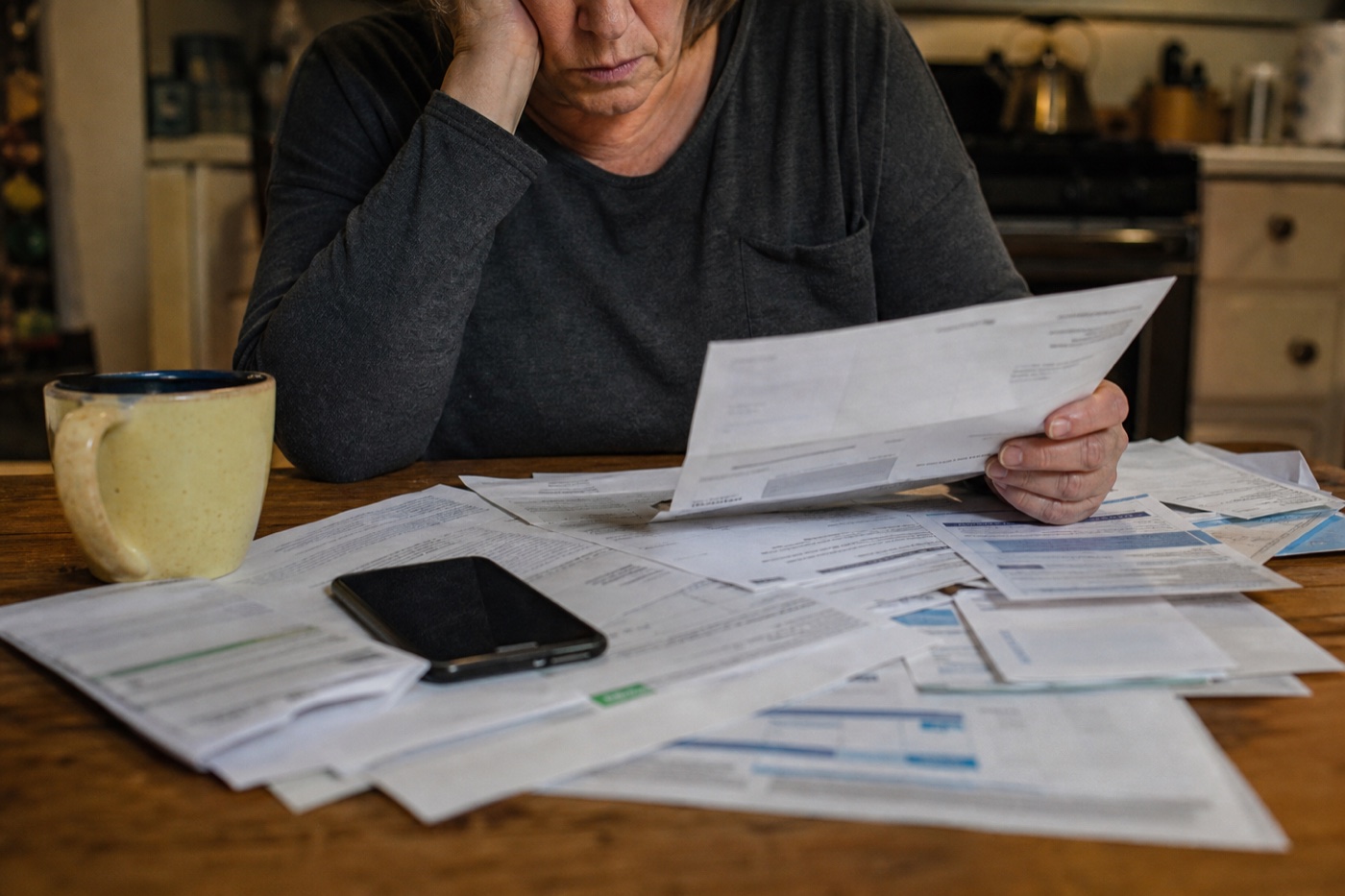

Missed a Premium? What a Lapse Really Means and What To Ask Fast

Life insurance does not usually end the day a payment is missed. Grace periods, reinstatement rules, and cash-value options give families more room than they think — if they ask quickly.

Covers policy renewals, final expense questions, auto and home coverage, and plain-English checklists for readers 55+.

Grace periods exist for exactly this situation

Most policies include a grace period after a missed payment, commonly around a month, during which coverage continues. The exact length is in the policy and can vary by state and policy type. If a payment was missed, the first call should be to the carrier to ask when the grace period ends and what amount brings the policy current.

Reinstatement is often possible, with conditions

After a lapse, many carriers allow reinstatement for a window of time. It usually requires paying the missed premiums and answering health questions again, and a new contestability period may apply. Reinstating an old policy is often better than buying a new one at an older age, but the carrier must confirm the terms in writing.

Cash value changes the options

Permanent policies with cash value may offer choices beyond simply lapsing: automatic premium loans, reduced paid-up coverage, or extended term coverage. Each has real tradeoffs, so ask the carrier to explain every nonforfeiture option listed in the policy before deciding.

- Ask for the current cash value and any outstanding policy loans.

- Ask what each nonforfeiture option would leave in place.

- Get the explanation in writing before choosing.

Watch for pressure to replace instead of fix

A caller who learns a policy is struggling may push a brand-new policy as the easy answer. Replacement restarts waiting periods and can cost more at an older age. Fixing the existing policy is often the cheaper path, and a licensed agent should be willing to compare both in plain language.

Where to verify this yourself

These official and consumer-protection sources cover the programs and rules discussed above. Rules change, so check the current version before acting.

Was this checklist useful?

One anonymous answer per reader. Results guide the editorial desk and are not displayed publicly until enough real votes exist.